Businesses need more than just a formula to understand how to track the depreciation of fixed assets. They need accurate, current asset records that show purchase cost, useful life, location, custodian, condition, maintenance history, and disposal status. Depreciation is easy to calculate, but hard to track when asset data changes faster than records are updated.

Introduction

Calculating fixed asset depreciation looks simple. All you need is the purchase cost of the asset, its useful life, depreciation method, acquisition date, and sometimes salvage value. From there, the finance department can apply a formula and build a depreciation schedule.

The harder part is keeping that schedule accurate as the asset moves through real business operations.

A forklift may transfer between sites. A laptop may be reassigned twice. A medical device may be repaired, stored, upgraded, or retired before finance sees the update. A machine may still be depreciating in a spreadsheet even though operations have already replaced it. This is where fixed asset depreciation becomes less of a calculation problem and more of an asset visibility problem.

For enterprise companies, fixed assets are long-term investments that affect books, budgets, taxes, audits, replacement planning, and operational readiness. But depreciation tracking is only as reliable as the asset data behind it.

The formula may be clean. The asset lifecycle rarely is.

That is why learning how to track depreciation for fixed assets requires a lifecycle-aware process. Finance needs accurate depreciation schedules, but operations, facilities, IT, and equipment teams create much of the day-to-day asset data that keeps those schedules trustworthy.

What does fixed asset depreciation actually mean?

Fixed asset depreciation is the process of spreading the cost of a physical asset over the period it is expected to be useful to the business.

Instead of recording the full cost of an asset as a one-time expense, businesses allocate that cost over the asset’s useful life. This reflects the idea that assets lose value as they age, wear down, become obsolete, or are consumed through use.

Common depreciable fixed assets include:

- Machinery

- Vehicles

- Computers and IT equipment

- Furniture

- Tools

- Medical equipment

- Production equipment

- Facilities equipment

- Specialized operational devices

For example, if a company buys a piece of equipment that will support operations for five years, depreciation helps spread that cost across those five years. This gives the business a clearer view of asset value, cost allocation, replacement timing, and financial reporting.

Depreciation is often treated as an accounting task, but it also has operational value. It helps leaders understand which assets are aging, which assets may need replacement, and where capital planning should happen next.

Depreciation rules can vary by jurisdiction, accounting policy, and asset class, so teams should always confirm financial treatment with their accounting or tax advisors. The operational principle, however, remains consistent: depreciation is most useful when it is tied to accurate, current asset records.

Why is the depreciation calculation usually the easy part?

The process of calculating depreciation is usually straightforward because most methods rely on a few defined inputs, such as cost, useful life, salvage value, acquisition date, disposal date, and depreciation method.

In many cases, the formula itself is not the problem. The challenge is whether the data feeding the formula is complete and up to date.

The core inputs usually include:

| Input | Why it matters |

| Purchase cost | Establishes the asset’s starting value |

| Useful life | Defines how long the asset will be depreciated |

| Salvage value | Estimates the asset’s residual value at the end of use |

| Depreciation method | Determines how depreciation is calculated over time |

| Acquisition date | Starts the depreciation timeline |

| Disposal or retirement date | Helps stop or update depreciation when the asset leaves service |

Two common fixed asset depreciation methods are straight-line depreciation and declining balance depreciation.

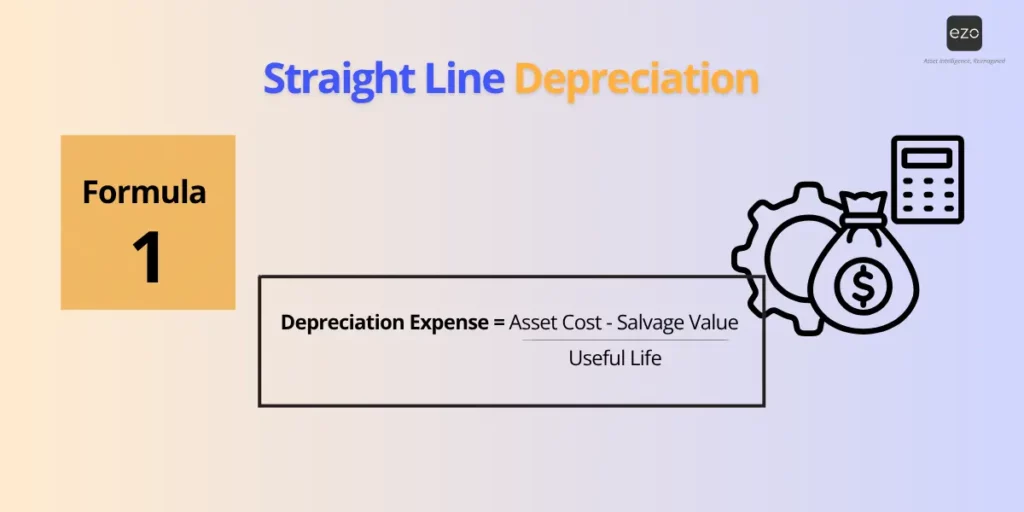

What is straight-line depreciation?

Straight-line depreciation spreads an asset’s cost evenly across its useful life, making it one of the simplest methods to calculate. The challenge is not the formula, but keeping the asset record accurate as the asset moves, gets repaired, changes ownership, or is retired.

For example, if a $10,000 asset has a five-year useful life and no salvage value, straight-line depreciation would allocate $2,000 of depreciation per year.

This method is popular because it is simple, predictable, and easy to audit.

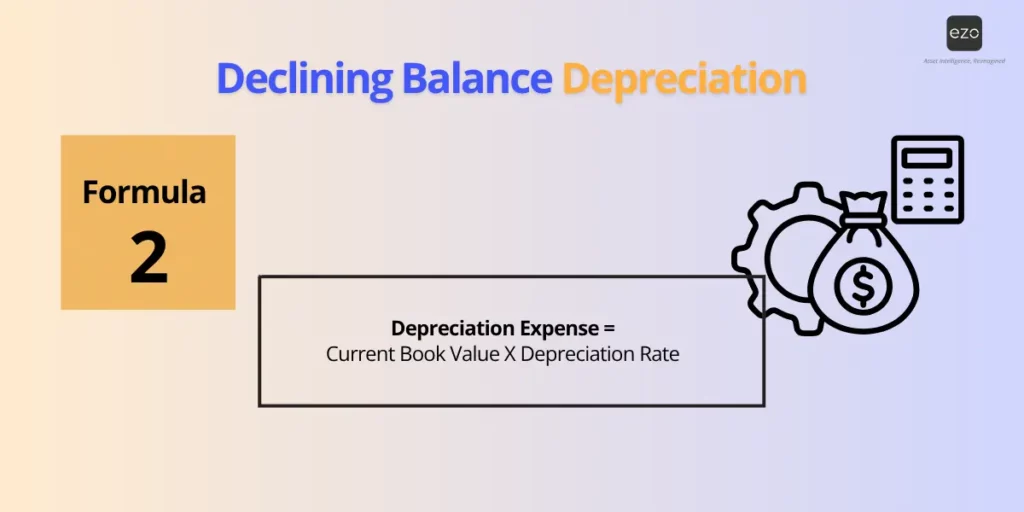

What is declining balance depreciation?

Declining balance depreciation records more depreciation earlier in the asset’s life and less depreciation later. This method can be useful for assets that lose value faster in the first few years.

EZO’s depreciation documentation states that EZO supports straight-line and declining-balance depreciation methods at the group level, and that users can enable them through the Asset Depreciation add-on. EZO also notes that users can run straight-line and declining-balance models, including both methods simultaneously when needed.

The point is not that every business needs a complex depreciation calculator. The point is that depreciation tracking becomes reliable when the method is supported by accurate asset records.

Why is fixed asset depreciation hard to track in real life?

Fixed asset depreciation is hard to track because an asset’s useful life keeps changing, even when the depreciation schedule remains static.

A spreadsheet may show a clean depreciation timeline. But the asset itself may be moving through a much messier lifecycle.

Assets move between locations. Employees change roles. Departments transfer custody. Equipment gets repaired, upgraded, damaged, stored, or replaced. Some assets are used heavily every day, while others sit idle for months. Some are physically retired before they are removed from the active asset register.

That means depreciation data can quickly become disconnected from operational reality.

For example, a production machine may still be depreciating on the books, but it may have been moved to another facility, repaired multiple times, fitted with a replacement component, taken offline for maintenance, and eventually replaced by newer equipment. If those lifecycle changes are not reflected in the asset record, the depreciation schedule may still appear mathematically correct yet be disconnected from the asset’s actual operational value.

This is especially difficult for companies managing fixed assets across multiple offices, warehouses, job sites, departments, or teams. Finance may have one version of the asset register. Operations may have another. IT, facilities, or equipment managers may rely on their own spreadsheets.

The result is a depreciation process that technically calculates value but does not always reflect the asset’s real status.

In our experience, this is where teams start losing trust in their own reports. The formula works, but the data does not.

What are the biggest tracking gaps that distort depreciation data?

The biggest tracking gaps are incomplete asset records, poor custody tracking, delayed disposal updates, spreadsheet dependency, and disconnected maintenance history.

These gaps distort depreciation data because they prevent finance and operations from working from the same version of asset truth.

Missing or incomplete asset records

Depreciation tracking starts with bad data when the purchase cost, acquisition date, serial number, category, useful life, or depreciation method is missing.

Even one missing field can create downstream reporting issues. If the purchase date is wrong, the depreciation timeline may be wrong. If the category is missing, useful life assumptions may be inconsistent. If the serial number is not recorded, teams may struggle to verify the asset during an audit.

Poor location and custody tracking

If the company does not know where an asset is or who has it, finance may continue depreciating assets that are missing, idle, replaced, or no longer in use.

Custody tracking is not just an operational concern. It helps validate whether an asset still exists, who is responsible for it, and whether it continues to contribute value.

Delayed disposal records

Assets are often physically retired before they are removed from systems.

This creates inaccurate active asset registers and misleading depreciation reports. A machine may be sitting in storage, sold, scrapped, or replaced, yet still appear as active in financial records. This can affect audits, replacement planning, and asset valuation.

Manual spreadsheets

Spreadsheets can calculate depreciation, but they do not enforce asset workflows.

They do not automatically know when an asset moves, gets checked out, comes back damaged, receives maintenance, changes owners, or is retired. They also depend on people updating them on time, in the right format, and in the right version.

Spreadsheets are useful for formulas. However, they have no control over the asset lifecycle.

Disconnected maintenance history

Maintenance and depreciation are not the same thing, but they are connected.

A heavily repaired asset may need replacement sooner than expected. A well-maintained asset may stay productive longer. If maintenance history is disconnected from the asset record, managers lose context when deciding whether to repair, replace, or retire equipment.

EZO supports asset tracking, location history, assignments, check-in/check-out workflows, lifecycle management, reporting, analytics, and maintenance alerts, all of which help keep operational asset records up to date.

Why does depreciation tracking depend on the full asset lifecycle?

Depreciation tracking depends on the full asset lifecycle because every major asset event can affect the accuracy of depreciation records.

Fixed asset depreciation should not be treated as a standalone finance activity. It should be connected to how assets are requested, purchased, received, tagged, assigned, used, maintained, transferred, audited, retired, and disposed of.

Here is how lifecycle stages support more reliable depreciation tracking:

| Lifecycle stage | Why it matters for depreciation tracking |

| Request | Captures the business need behind the asset |

| Purchase | Establishes cost, vendor, acquisition date, and category |

| Receiving | Confirms the asset entered the organization |

| Tagging | Links the physical asset to a digital record |

| Assignment | Shows who is responsible for the asset |

| Usage | Helps validate whether the asset is active or idle |

| Maintenance | Adds condition and repair context |

| Transfer | Tracks location and department changes |

| Audit | Confirms physical existence and record accuracy |

| Retirement | Signals the asset may no longer be in productive use |

| Disposal | Helps stop or update depreciation tracking |

Fixed asset depreciation becomes more reliable when every major lifecycle event is captured in the same system that tracks the asset itself.

EZO describes asset lifecycle management as the process of managing an asset from planning through disposal, with enterprise goals including cost control, compliance, risk reduction, and operational continuity. That lifecycle view is important because depreciation data does not live in isolation. It depends on what is happening to the asset in the real world.

Who owns fixed asset depreciation tracking?

Fixed asset depreciation tracking is a shared responsibility between finance, operations, IT, facilities, equipment teams, and procurement.

Finance may calculate depreciation, but operations creates much of the data that makes depreciation accurate.

Finance

Finance needs accurate depreciation schedules, asset values, reporting, accumulated depreciation data, and disposal records. Without reliable asset data, financial reporting becomes harder to validate.

For example, if a generator was disposed of six months ago but still appears as active in the asset register, finance may continue depreciating an asset the business no longer owns or uses.

Operations

Operations knows whether equipment is being used, repaired, idle, damaged, missing, or replaced. This context helps determine whether the asset record still reflects reality.

For example, a packaging machine may still be listed as fully active, but operations may know it has been offline repeatedly due to breakdowns and is no longer reliable for production planning.

IT, Facilities, and Equipment teams

These teams often manage custody, checkouts, returns, assignments, physical condition, and asset movement. They are usually closest to the day-to-day lifecycle events that affect asset accuracy.

For example, a maintenance team may move a compressor from one site to another, or Facilities may retire old HVAC equipment after replacement. If these updates are not recorded, depreciation reports may show the right numbers against the wrong location or status.

Procurement

Procurement needs lifecycle and depreciation data to plan replacements, avoid unnecessary purchases, and understand when assets should be renewed or retired.

For example, if procurement cannot see that several forklifts are nearing the end of useful life and already require frequent repairs, they may delay replacement planning until equipment failure disrupts operations.

The key point is simple: depreciation tracking fails when only finance owns it.

A shared asset management system gives every stakeholder a clearer view of asset status. Finance gets cleaner records. Operations gets better visibility. Procurement gets better planning data. Leadership gets reports they can trust.

What are the signs that your depreciation tracking process is breaking down?

Your depreciation tracking process is breaking down when the asset register no longer matches physical inventory, reports require manual cleanup, and teams cannot confidently explain where assets are, who owns them, or whether they are still active.

Common warning signs include:

- The asset register does not match the physical inventory

- Finance has assets listed that operations cannot find

- Assets are still depreciating after disposal

- Teams buy replacements while older equipment is still marked active

- Audits require manual reconciliation

- Departments keep separate spreadsheets

- Maintenance history is not connected to asset records

- No one knows the current custodian

- Reports require manual cleanup before they can be trusted

- Depreciation schedules are updated only during annual reviews

- Assets are transferred without timely record updates

- Retired equipment remains in active reports

- Managers cannot easily see asset age, condition, and depreciation status together

These issues are not just accounting inconveniences. They affect budget planning, equipment availability, compliance readiness, audit preparation, and operational decision-making.

For enterprise companies, the risk grows with scale. A small discrepancy across a few assets may be manageable. But when hundreds or thousands of assets are spread across departments, locations, and custodians, manual reconciliation becomes slow, expensive, and unreliable.

How can businesses make fixed asset depreciation easier to track?

Businesses can make fixed asset depreciation easier to track by maintaining a clean asset register, tagging assets early, tracking custody and location changes, connecting maintenance data, recording disposals on time, and reviewing depreciation reports throughout the year. Let’s understand how businesses can make equipment depreciation tracking easier.

Start with a clean asset register

Every fixed asset should have a complete record that includes:

- Purchase date

- Purchase cost

- Asset category

- Serial number

- Location

- Owner or custodian

- Useful life

- Depreciation method

- Warranty details

- Maintenance history

- Retirement or disposal status

This provides finance and operations with a shared foundation for tracking asset depreciation over time.

Tag assets at purchase or receiving

Use barcodes, QR codes, RFID tags, or other identifiers to connect physical assets to digital records.

Tagging assets early reduces the risk of orphaned assets, duplicate entries, and audit confusion. It also makes it easier for teams to scan assets during checkouts, transfers, inspections, and audits.

Track custody and location changes

Depreciation tracking becomes more reliable when the organization can confirm whether the asset still exists, where it is, and who is responsible for it.

This is especially important for assets that move frequently between employees, departments, job sites, or storage areas.

Connect maintenance and condition data

Maintenance history helps teams decide whether an asset should continue in use, be repaired, or be replaced.

A depreciation schedule may say an asset has two years of useful life remaining. But if the asset has recurring breakdowns, rising repair costs, or poor availability, managers may need to replace it sooner.

Record retirements and disposals on time

Disposal should be part of the workflow, not an afterthought.

When an asset is retired, sold, scrapped, donated, or lost, that event should be captured quickly. Timely disposal records help prevent assets from staying active in reports after they have left service.

Use reports regularly, not only at year-end

Depreciation reports should be reviewed throughout the year, especially before audits, budgeting cycles, procurement planning, and compliance checks.

EZO’s asset depreciation documentation explains that users can manage depreciation across groups, generate reports, run straight-line and declining balance models, and configure depreciation at the group level. This kind of reporting helps teams move from occasional cleanup to ongoing asset visibility.

Why can spreadsheets calculate depreciation but not manage depreciation tracking?

Spreadsheets can calculate depreciation, but they cannot track it because they do not capture asset lifecycle events in real time.

A spreadsheet can be useful for:

- Formulas

- Small asset lists

- Simple depreciation schedules

- One-time analysis

- Basic reporting

But spreadsheets struggle when assets are actively moving through the business.

They are not designed to manage:

- Real-time updates

- Multi-location assets

- Custody changes

- Audit trails

- Check-in/check-out activity

- Maintenance history

- Disposal workflows

- Access control

- Mobile updates

- Reporting across departments

- Asset condition changes

- Lifecycle events from purchase to disposal

This is the difference between calculation and tracking.

A spreadsheet can tell you what an asset should be worth based on a formula. It cannot reliably tell you whether the asset is still in use, where it is, who has it, whether it was repaired last month, or whether it was retired but never removed from the active register.

That is why spreadsheets often create a false sense of control. The depreciation schedule may look complete, but the operational data underneath it may be outdated.

For growing businesses, this becomes a serious visibility gap. Teams need a system that connects depreciation tracking with the actual movement, use, maintenance, and disposal of assets.

How does EZO help track fixed asset depreciation?

EZO helps track fixed asset depreciation by connecting depreciation data with fixed asset records, lifecycle workflows, custody tracking, location visibility, maintenance history, reports, and audits.

It should not be positioned as a replacement for accounting software. Instead, it supports the operational side of depreciation tracking by helping finance and operations work from more accurate asset records.

For companies evaluating enterprise asset management software, this matters because depreciation tracking depends on the quality of asset data across the full lifecycle.

EZO supports fixed asset tracking, including asset availability, location, and depreciation. EZO also states that its depreciation functionality supports straight-line and declining balance methods at the group level. Its depreciation guide states that teams can manage depreciation across groups, draft reports, and run both straight-line and declining-balance methods as needed.

Here is how this helps teams track depreciation for fixed assets more reliably:

Finance gets cleaner depreciation records

Finance teams can work from centralized asset records instead of chasing updates across departments. Depreciation reports become easier to review when asset cost, category, useful life, and status are connected to the asset record.

Operations can validate asset status

Operations teams can confirm whether an asset is active, moved, assigned, idle, damaged, maintained, or retired. This helps prevent depreciation schedules from becoming disconnected from what is happening on the ground.

Managers can plan replacements with better context

Depreciation indicates how an asset’s value changes over time. But replacement planning also depends on age, condition, usage, maintenance, and availability. By connecting these records, managers can make more informed decisions about when to repair, replace, or retire assets.

Audits become easier to support

Centralized records, custody history, location data, and reports make it easier to validate the existence and status of assets. Instead of manually reconciling multiple spreadsheets, teams can use a shared system to support audit readiness.

Disposal decisions are easier to document

When assets are retired or disposed of, teams can update the asset lifecycle record. This helps ensure active asset reports and depreciation records do not continue to include assets that have already left service.

In short, EZO helps teams move from treating depreciation as a static financial schedule to treating it as part of a broader fixed asset management process.

Why is fixed asset depreciation not just about value, but visibility?

Fixed asset depreciation is not just about value because depreciation data only becomes useful when the business can see what is happening to the asset.

The formula may be simple. Tracking is difficult because asset data changes constantly.

An asset’s value on paper should not be disconnected from its real-world status. If an asset is missing, idle, transferred, damaged, heavily repaired, or retired, that context matters. Without it, depreciation reports can become technically accurate but operationally misleading.

The best process connects finance and operations. Finance owns the depreciation schedule, but operations helps keep asset records up to date. A centralized asset management system gives both teams a shared source of truth.

That is how to track depreciation for fixed assets with more confidence: connect depreciation schedules to the full asset lifecycle, from purchase to disposal.

Conclusion

Fixed asset depreciation is easy to calculate when the inputs are clean. But in real businesses, assets rarely stay still.

They move between sites, change custodians, undergo repairs, sit idle, get replaced, and eventually retire. If those lifecycle events are not captured, depreciation tracking becomes unreliable.

For enterprise companies, the goal is not just to calculate depreciation. The goal is to keep depreciation data tied to real asset status.

EZO helps teams manage fixed assets with better visibility across depreciation, custody, location, maintenance, reporting, audits, and lifecycle events. That gives finance, operations, and leadership a clearer way to understand asset value, plan replacements, and make better decisions.

![[How-to] Use Asset Depreciation in EZO](https://cdn.ezo.io/wp-content/uploads/2018/01/Depreciation-EZO-2.jpg)